Last week…the markets ended on a mostly down note.

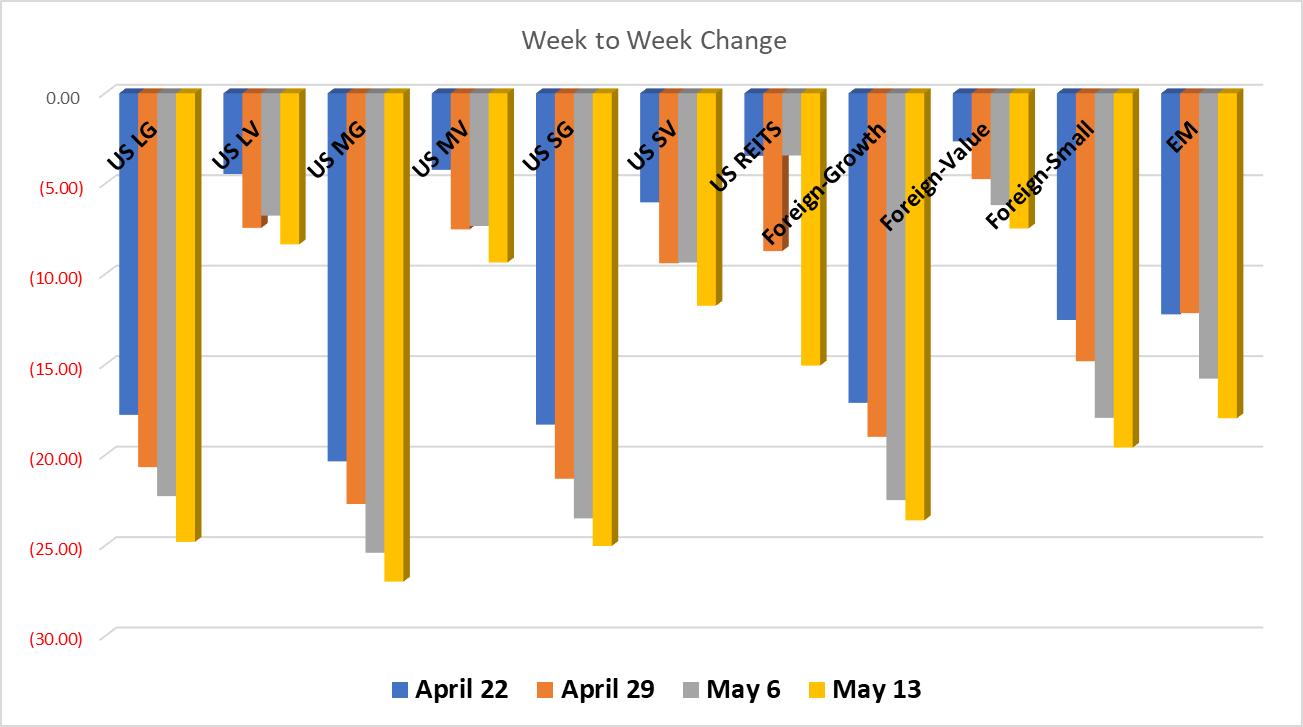

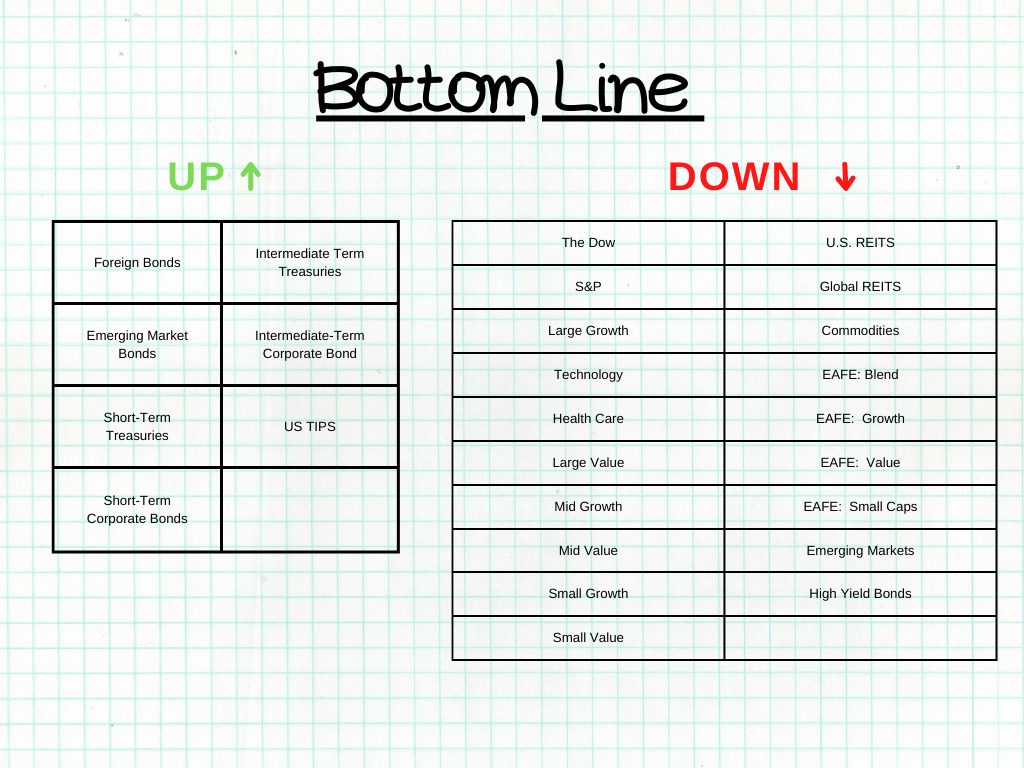

All US Equities were down. US Large Growth companies were down the most, followed by US Small Value and Technology. Last week there was no discernable pattern between Growth and Value nor between small, mid and large companies. Meaning, the markets were all over the place.

US REITS were down more than Global REITS, perhaps another side effect of rising interest rates and the cash flow in the US.

Commodities slipped a bit over 2% despite the rising gas prices at the pump.

Foreign Equities were also down, but not quite as much as the US. Emerging Markets continued their downward trend.

Bonds were slightly more exciting last week. US High Yield was down over 1%, but the rest of bonds were up. Foreign Bonds were up for the first time in many weeks. US Short Term Treasuries and Corporates were up 0.3% and 0.15% respectively. Intermediate Term Treasuries and Corporates were up 0.65% and 0.45% respectively. And finally, TIPS were up over 0.3%.

Have a great weekend!

All performance reported in the graph and performance references are from the following index list: DJ Industrial Average TR USD, S&P 500 TR, DJ US TSM Large Cap Growth TR USD, NASDAQ 100, Technology NTTR TR USD, DJ US Health Care TR USD, DJ US TSM Large Cap Value TR USD, DJ US TSM Mid Cap Growth TR USD, DJ US TSM Mid Cap Value TR USD, DJ US TSM Small Cap Growth TR USD, DJ US TSM Small Cap Value TR USD, FTSE NAREIT All Equity REITs TR, DJ Gbl Ex US Select REIT TR USD, Bloomberg Commodity TR USD, MSCI EAFE NR USD, MSCI EAFE Growth NR USD, MSCI EAFE Value NR USD, MSCI EAFE Small Cap NR USD, MSCI EM NR USD, BBgBarc US Corporate High Yield TR USD, FTSE WGBI NonUSD USD, JPM EMBI Plus TR USD, BBgBarc US Govt 1-3 Yr TR USD, ICE BoafAML 1-3Y US Corp TR USD, BBgBarc Intermediate Treasury TR USD, BBgBarc Interm Corp TR, BBgBarc US Treasury US TIPS TR USD. This material has been prepared solely for informational purposes based upon data generally available to the public from sources believed to be reliable. All performance reporting is for indexes, not specific securities. Performance of specific securities will vary from indexes. Past performance is not an assurance of future results. Indexes cited are provided to illustrate market trends for certain asset classes. It is not possible to invest directly in an index. Indexes do not reflect individual investor costs of trading, expense ratios & advisory or other fees