Last week…

…the markets clawed back some ground.

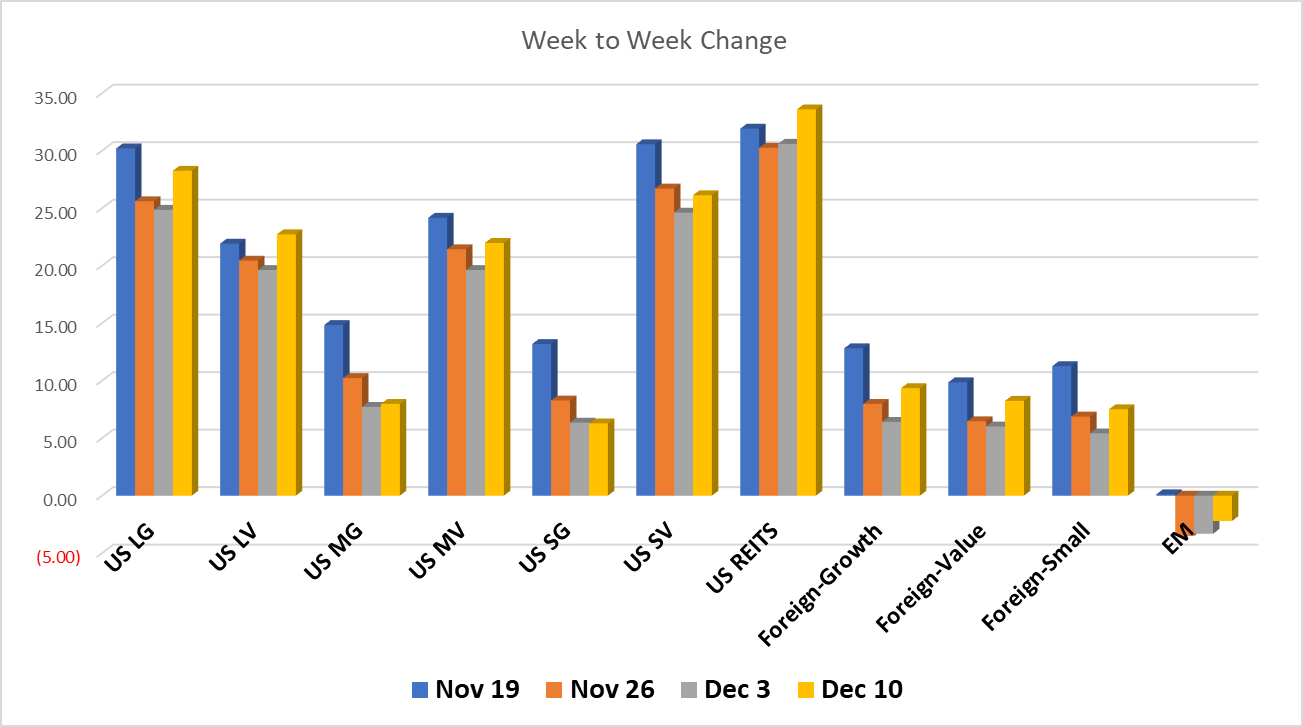

As illustrated in the graph, most asset classes had a major comeback last week, not quite returned to previous highs, but a positive move nonetheless.

US Large Cap companies saw the biggest surge with growth and value both up over 3%. Technology had the biggest gain of nearly 5%. Remember last week Tech was down the most? Technology is now nearing a 40% return YTD. Mid Caps and Small Caps exhibited similar patterns with each showing value outperforming growth.

REITS both US and Global were up over 2% from the previous week. Commodities also moved forward.

Foreign Equities also had a stellar week with everything up over 2%. It is noteworthy that Foreign Small Caps did a bit better than US. Emerging Markets are still hovering below water, but was up from last week.

And once again, Bonds didn’t give us anything worth writing home about!

Have a great weekend!

All performance reported in the graph and performance references are from the following index list: DJ Industrial Average TR USD, S&P 500 TR, DJ US TSM Large Cap Growth TR USD, NASDAQ 100, Technology NTTR TR USD, DJ US Health Care TR USD, DJ US TSM Large Cap Value TR USD, DJ US TSM Mid Cap Growth TR USD, DJ US TSM Mid Cap Value TR USD, DJ US TSM Small Cap Growth TR USD, DJ US TSM Small Cap Value TR USD, FTSE NAREIT All Equity REITs TR, DJ Gbl Ex US Select REIT TR USD, Bloomberg Commodity TR USD, MSCI EAFE NR USD, MSCI EAFE Growth NR USD, MSCI EAFE Value NR USD, MSCI EAFE Small Cap NR USD, MSCI EM NR USD, BBgBarc US Corporate High Yield TR USD, FTSE WGBI NonUSD USD, JPM EMBI Plus TR USD, BBgBarc US Govt 1-3 Yr TR USD, ICE BoafAML 1-3Y US Corp TR USD, BBgBarc Intermediate Treasury TR USD, BBgBarc Interm Corp TR, BBgBarc US Treasury US TIPS TR USD. This material has been prepared solely for informational purposes based upon data generally available to the public from sources believed to be reliable. All performance reporting is for indexes, not specific securities. Performance of specific securities will vary from indexes. Past performance is not an assurance of future results. Indexes cited are provided to illustrate market trends for certain asset classes. It is not possible to invest directly in an index. Indexes do not reflect individual investor costs of trading, expense ratios & advisory or other fees