Last Week…

… Cautious optimism continued

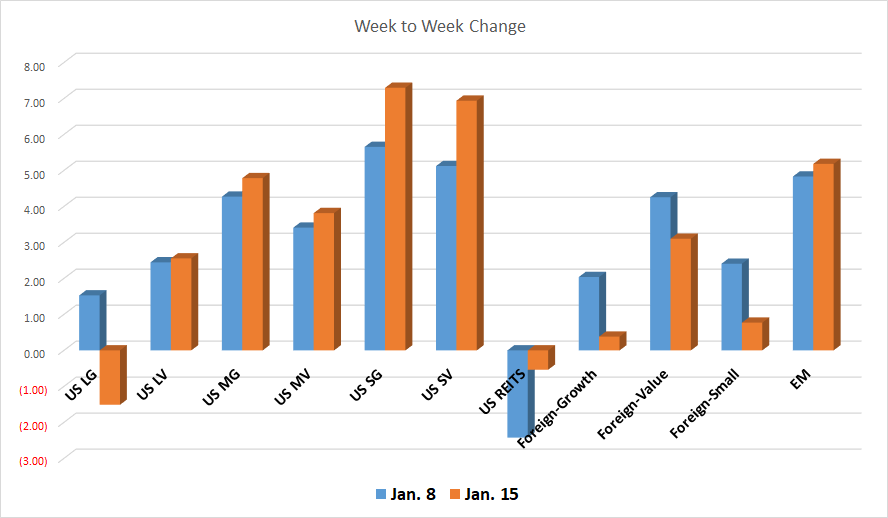

US Small Companies are streaking ahead of Large US companies with Value continuing to outperform Growth.

- US Small stocks skipped ahead again by another 1.6% and 1.8 but, stood near 7.0% YTD!

- While Large Growth stocks remain negative -1.5% with Large Value up 2.6%

- REITS looked a bit different.

-

- US REITS surged ahead 1.89% but remains negative YTD

- Global REITS dropped another -1.43%

- Commodities are finally back in the black – not only YTD but, for the one, two and five year trailing returns!

Foreign Stocks were mostly down on the week but all remain positive YTD with Large Value performance outstripping Large Growth tenfold. The weekly trend saw:

- Large Growth -1.66%

- Large Value -1.15%

- Small Cap -1.64%

Bonds Bobbled like a fishing line float

- Tips saw the most progress +0.45%

We shall see if the market myth “As January goes so goes the year” holds true in 2021.

Have a great weekend!

Indexes are listed in respective order to their reference above: DJ Industrial Average TR USD, S&P 500 TR, DJ US TSM Large Cap Growth TR USD, NASDAQ 100, Technology NTTR TR USD, DJ US Health Care TR USD, DJ US TSM Large Cap Value TR USD, DJ US TSM Mid Cap Growth TR USD, DJ US TSM Mid Cap Value TR USD, DJ US TSM Small Cap Growth TR USD, DJ US TSM Small Cap Value TR USD, FTSE NAREIT All Equity REITs TR, DJ Gbl Ex US Select REIT TR USD, Bloomberg Commodity TR USD, MSCI EAFE NR USD, MSCI EAFE Growth NR USD, MSCI EAFE Value NR USD, MSCI EAFE Small Cap NR USD, MSCI EM NR USD, BBgBarc US Corporate High Yield TR USD, FTSE WGBI NonUSD USD, JPM EMBI Plus TR USD, BBgBarc US Govt 1-3 Yr TR USD, ICE BoafAML 1-3Y US Corp TR USD, BBgBarc Intermediate Treasury TR USD, BBgBarc Interm Corp TR, BBgBarc US Treasury US TIPS TR USD. These materials have been prepared solely for informational purposes based upon data generally available to the public from sources believed to be reliable. All performance references are to benchmark indexes. Performance of specific funds will vary from respective benchmarks. Past performance is not an assurance of future results. Each index cited is provided to illustrate market trends for various asset classes. It is not possible to invest directly in an index. Neither do Indexes reflect individual investor costs, e.g. trading, expense ratios & potential advisory fee.